For Emini Equity Index

Simple Calibration

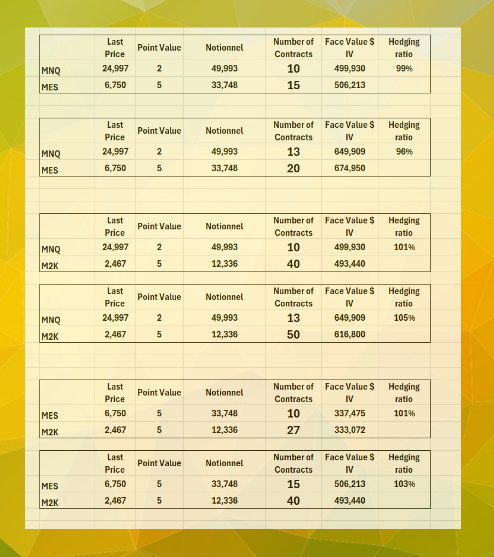

Calibrating 2-Leg Strategies on Equity Index

Mastering Micro & Mini Contracts for Safer Futures Trading

Updated on 6th Oct. 25. This Calibration is correct until next update

In futures trading—especially when working with equity index spreads like the S&P 500 (ES), Nasdaq 100 (NQ), and Russell (RTY)—capital preservation and risk control must be our top priorities. One of the most effective ways to achieve that is by using micro and mini contracts strategically.

👉 Remember: Not all traders need to go full size. In fact, most of us shouldn't—especially when our goal is to stay in the game over the long term. That’s where micro and mini contracts come in.

🎯 Why Micro and Mini Contracts Matter

Contracts in futures are standardized—but they come in different point values, which means different exposures. To tailor position size to our account size, we should aim to work as often as possible with mini and micro contracts.This gives us two key advantages: We can size our positions more precisely. We can better manage risk without being overexposed.

🛠️ Example: Mixing Contracts for Smarter ExposureYou don’t need to stick to only minis or only micros.

You can mix them to get closer to your ideal size:10 Micro E-mini S&P 500 contracts = 1 E-mini S&P 500 contract15 Micro E-mini S&P contracts = 1 Mini + 5 MicrosThis logic can be applied the same way with Nasdaq (NQ) and Russell (RTY) contractsBy thinking in combinations, you gain flexibility and control. That’s how pros scale exposure without unnecessary risk.

✅ Coaching Takeaway:Trading is not about going big. It’s about going smart.✔ Use micro and mini contracts to scale responsibly

✔ Combine contract sizes to customize your position

✔ Focus on point value equivalence, not price

✔ Always trade in a way that respects your capital and risk profile